Monira Aloud

Monira Aloud

580 California St., Suite 400

San Francisco, CA, 94104

2016

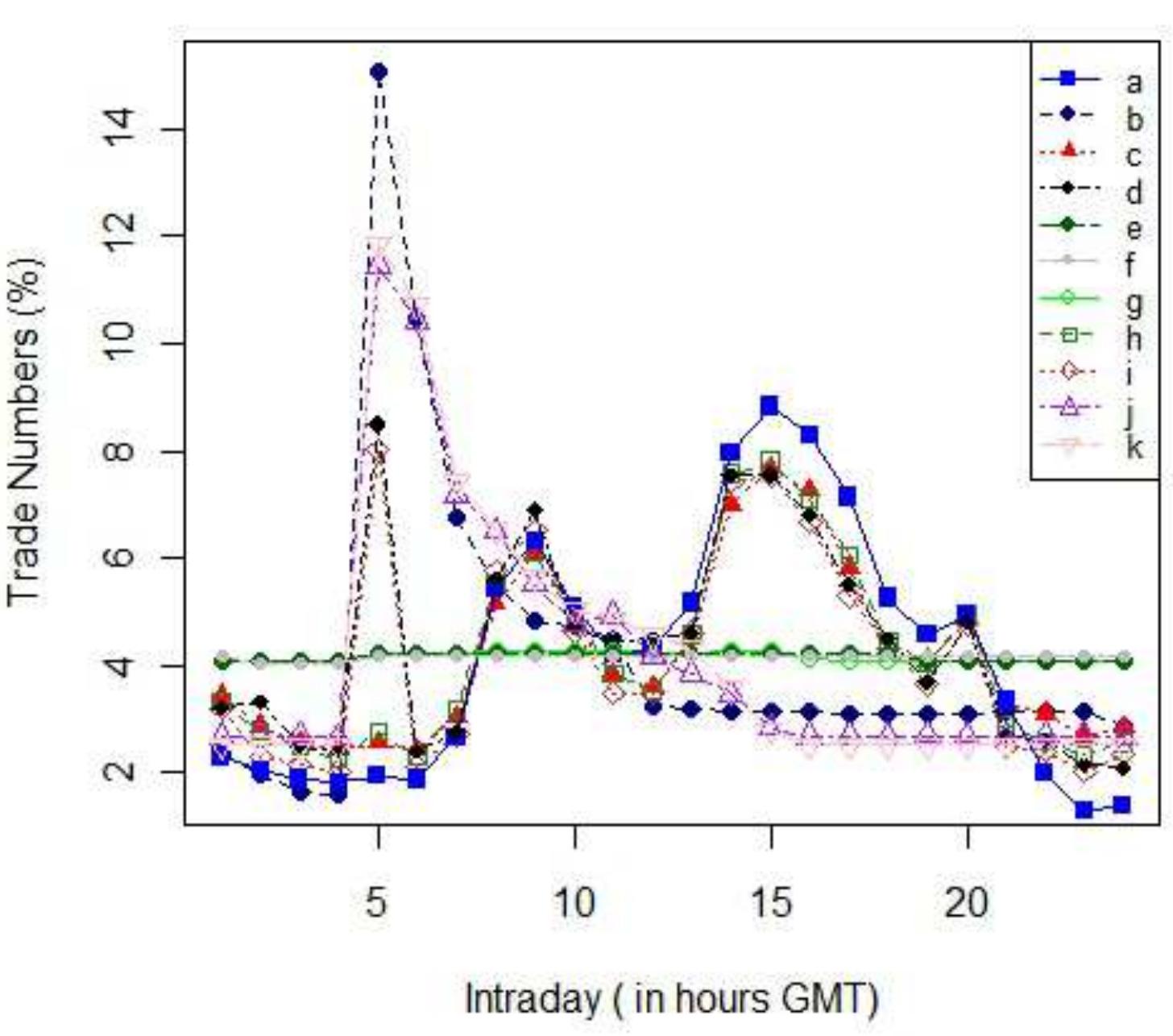

One of the most critical issues that developers face in developing automatic systems or software agents for electronic markers is that of endowing the agents with appropriate trading strategies. In this paper, we examine the problem in the Foreign Exchange (FX) market and we use an agent-based FX market simulation to examine which trading strategies lead to market states in which the stylized facts (statistical properties) of the simulation match the stylised facts of the actual FX market transactions data. In particular, our goal is to explore the emergence of the stylized facts of the transactions data, when the simulated market is populated with agents using three different strategies: a variation of the zero-intelligence with a constraint (ZI-CV) strategy; the zero-intelligence directional-change event (ZI-DCT0) strategy; and a genetic programmingbased (GP) strategy. A series of experiments were conducted in an existing agent-based FX market with these three strategies and the r...